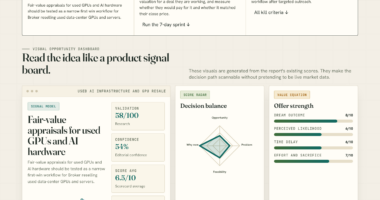

📊 Full opportunity report: The queue. Why the grid, not the chip, is the binding constraint on AI. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

The primary bottleneck for AI infrastructure buildout has shifted from semiconductor supply to the grid connection process. The interconnection queue delays projects by years, leading to private, behind-the-meter power solutions that externalize costs onto ratepayers.

The main constraint on AI infrastructure growth in the US has shifted from semiconductor chips to the power grid connection process, with the interconnection queue now delaying thousands of gigawatts of projects by years.

Over the past two years, the narrative centered on chip shortages and GPU availability. Today, the bottleneck is the grid, specifically the interconnection queue, where approximately 2,300 to 2,600 gigawatts of generation and storage projects are waiting for connection approval. The median wait time has increased from under two years in 2008 to nearly five years now, with some projects facing up to twelve-year delays, according to industry sources.

This demand surge is unprecedented: US data-center power demand is projected to reach 76 gigawatts in 2026, up from 50 gigawatts in 2024, while global data-center consumption could surpass 1,000 terawatt-hours annually by the early 2030s. Utilities report more gigawatts of data-center applications than their maximum historical peak demands. In Texas, requests for large interconnections increased 700% in a single year, from 1 gigawatt to 8 gigawatts, illustrating the scale of the demand.

As a result, capital is bypassing the grid. Behind-the-meter gas plants and co-located nuclear facilities are being built to supply power immediately, with some projects claiming to reach commercial operation within 18 months, while grid access remains years away. Major corporations like Microsoft are even restarting nuclear plants like Three Mile Island to secure baseload power, bypassing transmission delays entirely. Meanwhile, utilities report that more gigawatts of applications now exceed their traditional peak demands, leading to increased costs and political tensions, especially over who bears the financial burden of expanding and upgrading the grid infrastructure.

The queue.Why the grid, not the chip,

is the binding constraint on AI.

more than total installed capacity

up to 12 years for data centers

vs grid access maybe 2035

ratepayers · the cost-shift, concrete

in a single year

Virginia ratepayers (2024)

across PJM consumers

The grid is the bottleneck. The private grid is the response. And the seam between them — who pays for the public infrastructure the private builders still lean on — is where the economics and politics of the AI buildout are now decided.Thorsten Meyer · The Queue · AI Energy & Infrastructure 02

Implications of the Interconnection Queue Shift

This shift reflects a change in the challenges faced in deploying AI infrastructure. The bottleneck in grid connection is influencing project strategies, with some developers opting for private power sources to meet immediate needs. The increased costs associated with expanding the grid are often passed on to consumers and ratepayers, which may influence future energy policies and regulatory approaches.

Westinghouse 12500 Watt Dual Fuel Home Backup Portable Generator, Remote Electric Start, Transfer Switch Ready, Gas and Propane Powered

- Power Output: 9500W running, 12500W peak (gas)

- Fuel Options: Gasoline and propane powered

- Start Type: Remote electric and recoil start

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

From Chip Shortages to Grid Constraints

For two years, the dominant story in AI infrastructure was chip shortages, driven by GPU scarcity and supply chain issues. As chip supply stabilized, attention shifted to the physical infrastructure needed to power AI expansion. The US’s interconnection queue emerged as the critical bottleneck, with the volume of pending projects far exceeding current grid capacity. Unlike the rapid pace of capital deployment in AI and data centers, grid connection times have extended from under two years in 2008 to nearly five years today, with some projects experiencing delays of up to twelve years.

This disparity has led to a strategic response: developers are building private power sources to meet immediate needs, effectively circumventing the grid. Meanwhile, the existing grid infrastructure struggles to keep pace, and the costs of expanding it are increasingly passed onto consumers and ratepayers, raising questions about cost distribution and regulatory oversight.

“The interconnection queue is now the primary constraint on AI infrastructure growth, shifting the focus from chips to the grid itself.”

— Thorsten Meyer

ECO WORTHY 10000W Output Complete Off-Grid Solar Panel Kit for Home| 10KW 120V/240V Output Split Phase Inverter| 48V 314Ah16.1kWh High Capacity Energy Storage| 2950W Solar Panel PV| Whole House System

- Power Output: 10kW with split-phase support

- Solar Panels: 5 × 590W panels, 2950W capacity

- Energy Storage: 48V 314Ah LiFePO₄ battery, 16.1 kWh

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Uncertainties in Future Grid Expansion and Policy Responses

The timeline for expanding grid infrastructure to meet rising demand remains uncertain, and policy measures addressing cost sharing and process improvements are still under discussion. The ongoing debate involves stakeholders from government, utilities, and industry, with no definitive resolutions at this stage.

POKIPO Large Power Tool Organizer Wall Mount with Charging Station,4 Layer Heavy Duty Metal Tool Storage Rack Loads 600lbs with 8 Cordless Drill Holder,Battery Utility Rack Loads with 4 Power Strip

- Integrated 4-Outlet Power Strip: Includes 4 outlets with 6.5-foot cord

- Supports 600lbs Load Capacity: Heavy-duty metal construction for durability

- 4-Tier Multi-Function Rack: Holds drills, batteries, tools, and accessories

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps in Addressing the Grid Constraint Challenge

Private developers are likely to continue investing in behind-the-meter solutions to mitigate delays. Simultaneously, policymakers and utilities may pursue initiatives to streamline interconnection procedures and develop strategies for shared cost allocation. Monitoring these developments will be important for understanding how the situation evolves and how industry and policy responses adapt.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why has the focus shifted from chips to the grid?

The interconnection queue now delays thousands of gigawatts of projects by years, making grid access the primary bottleneck for AI infrastructure expansion.

What are private power solutions, and why are they being built?

Private power solutions, such as behind-the-meter gas plants and co-located nuclear facilities, are being constructed to provide immediate power and bypass the lengthy grid connection process.

Who bears the costs of expanding the grid?

Cost externalization means that ratepayers and the public often bear the financial burden of grid upgrades, which can influence policy discussions and regulatory decisions.

How might this shift impact AI development timelines?

While private solutions can accelerate some projects, delays in grid expansion could still affect the broader deployment of AI infrastructure if scalable solutions are limited.

What policy measures could address the interconnection bottleneck?

Potential measures include streamlining permitting processes, increasing grid capacity, and establishing cost-sharing mechanisms to reduce delays and financial burdens on ratepayers.

Source: ThorstenMeyerAI.com